Carmignac P. EM Debt: Letter from the Fund Managers

Carmignac P. EM Debt lost -1.88% in the third quarter of 2023, while its reference indicator1 was down -0.94%.

Market environment

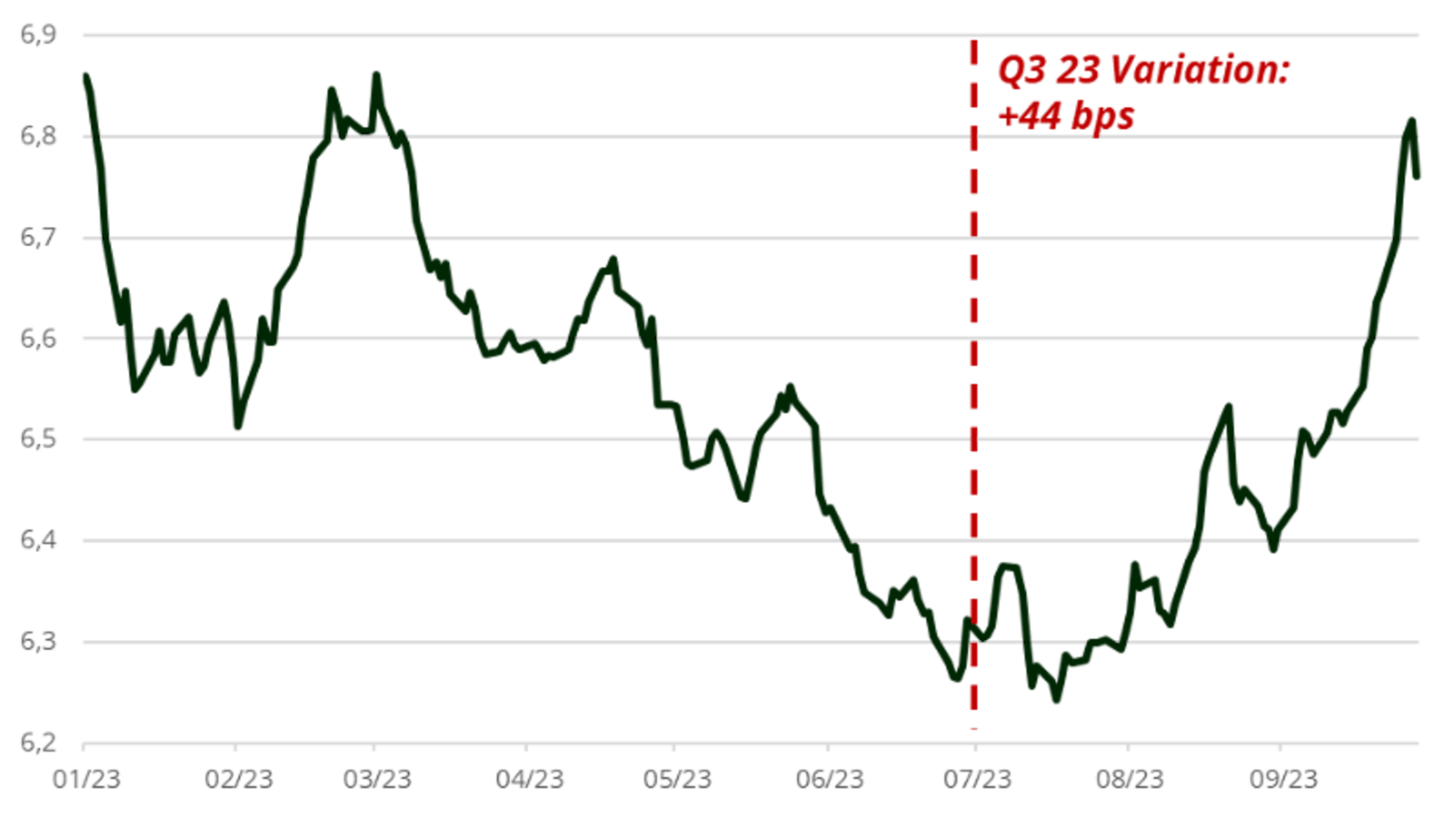

The third quarter of 2023 has been characterized by higher global rates and a volatile environment. Indeed, despite the potential last rate hike from the European Central Bank (ECB) and a pause from the Federal Reserve (Fed), the hawkish speeches from central bankers pushed the 10-year Treasury from around 3.84% to over 4.57%, and the German 10-year from around 2.39% to over 2.84%, reaching the highest levels of the year. Indeed, energy, which was one of the main sources of disinflation, is therefore set to become a positive contributor to price rises again by the end of the year, following the decision by the OPEP (mainly driven by Russia and Saudi Arabia) to extend their production cuts. This will penalize household purchasing power, but will also slow inflation's return to the central banks' targets.

Germany and US 10-year rates evolution

Sources: Carmignac, Bloomberg, 30/09/2023

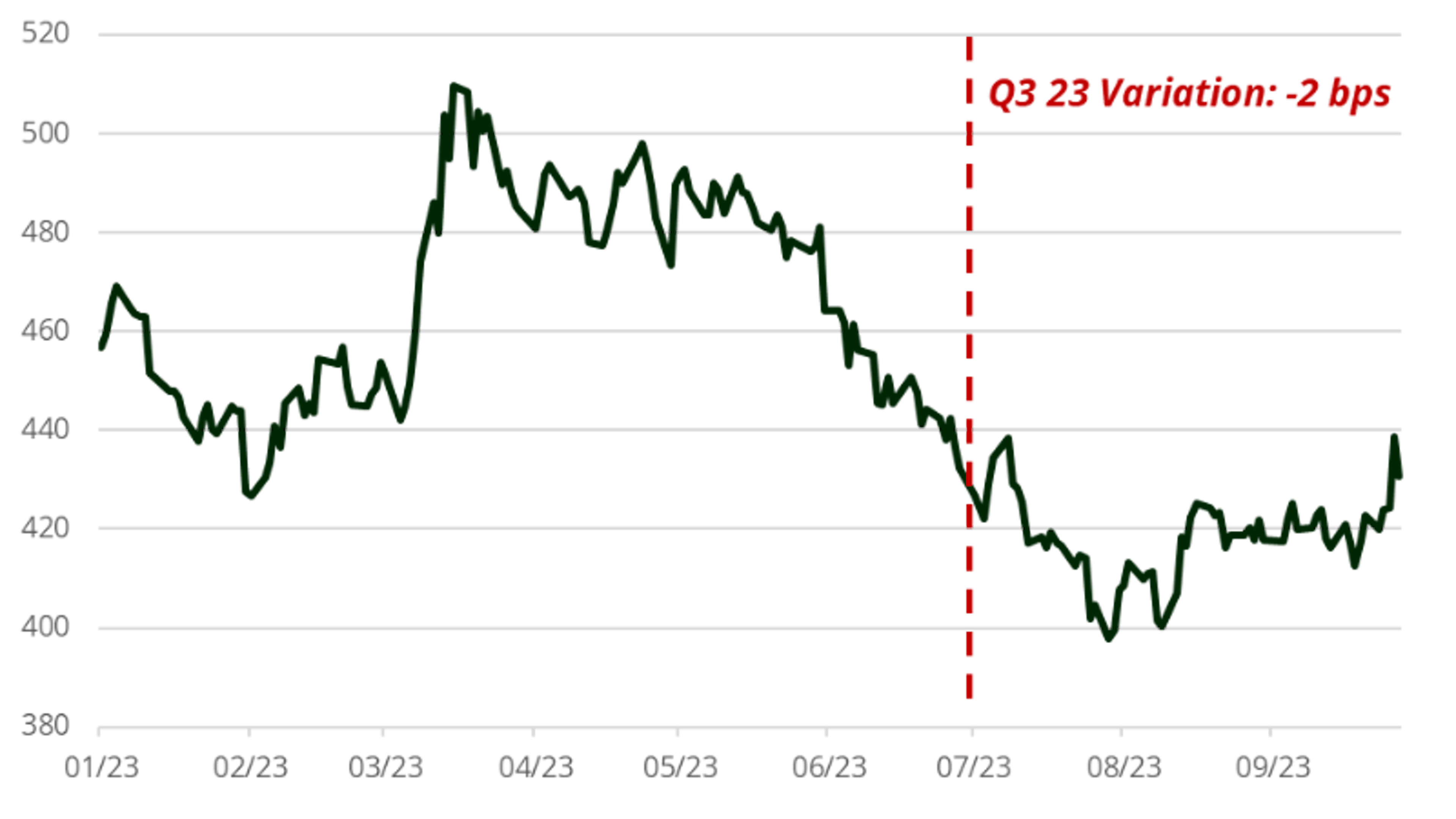

In terms of local rates, we continue to see rate cuts in the emerging market (EM) universe this quarter with notably Poland cutting by 75 basis points from 6.75% to 6%, surprising the market. The majority of Latin American countries have already begun to lower their rates, but they are doing so cautiously, as they are no longer in line with the Fed's policy of "higher rates for a longer period". In China, the disappointing reopening continues to linger. The country is faced with a more difficult international environment due to the desire of many nations to regain industrial sovereignty and the United States to hinder Chinese development. Investors grew more pessimistic about the country’s economic outlook.

GBI-EM Index (Local sovereign debt index) - Yield Evolution

Sources: Carmignac, Bloomberg, 30/09/2023

Furthermore on FX, EM currencies continued to attract investors. Commodity exporter currencies and high carry currencies like those in Latin America remained appealing. Nevertheless, a selective approach is still required, keeping an eye out for balance of payments and inflation trajectories. As an example, the CLP has experienced a decline for three consecutive months due to the challenges encountered by the Banco Central de Chile in maintaining stable interest rates, particularly in light of the rapid decline in inflation within the Chilean economy.

On sovereign credit, spreads remained stable over the period. Spreads were very tight in both the IG and HY spaces (distress names excluded) and the market kept a close eye on special situations such as in African countries. The sweet spot of this area remains in the BBs in which you can find the most attractive risk/reward opportunities.

J.P Morgan EMBIG diversified hedged EURO index (External sovereign debt index) - Spread

Sources: Carmignac, Bloomberg, 30/09/2023

What have we done in this context?

In this context we have mainly been impacted by our exposure to Local Rates in CZK, HUF, COP, MXN and CLP curves. The rise in US interest rates and the dollar, combined with the Chinese slowdown and rising inflation, have prompted us to reduce the risk in the portfolio. We notably reduced our exposure to the EMEA region, where valuations are not attractive as they were.

In the FX space we continue to enjoy the carry of EM FX currencies over the quarter. Nevertheless, on a risk management basis, we reduced our exposure to EM currencies and we continue to be selective and active in this segment. As an example, during the quarter we notably reduced our CZK exposure, which is directly impacted by oil imports. Following volatility peaks and increased in DM rates, we also increased our EUR exposure over the quarter.

On sovereign credit, we benefited from our exposure to the EMEA region, in particular through Romania. Lastly, over the period we increased on a tactical basis our exposure to Colombia as the country should benefit from the current trend on oil.

Outlook for the next months

Our view of recession and high rates is reflected in our portfolio construction, namely a large reduction of risky assets and a high level of CDS protections. We remain focused on duration with the view that a recession would force DM central banks to cut rates and thus enable further cuts in the EM world.

In Local Rates, we are closely monitoring EM Central banks to pursue their cutting cycles as the FED and ECB seem to have paused. We are ready to re-engage in countries which were among the most advanced in their rate hike cycle and in commodity exporters such as Colombia.

In Sovereign Credit, we continue to favour manufacturing countries that will benefit in the long term from the “nearshoring” phenomenon, i.e. the potential repatriation of production chains to closer and more stable countries (Romania, Poland, Mexico, etc.). Nevertheless, we remain cautious with protection against our HY names and will keep our positioning light and focused on the IG space.

Lastly, although we have reduced our global exposure to EM FX, we continue to favour a selection of currencies on a tactical/opportunist basis mainly in LATAM such as the Brazilian real and the Mexican peso.

Carmignac Portfolio EM Debt

Exploit fixed income opportunities across the entire emerging universeRecente analyses

![[Background image] [CI] Blue sky and buildings](https://carmignac.imgix.net/uploads/article/0001/05/CI_WEB.jpg?auto=format%2Ccompress&fit=fill&w=3840)

Carmignac Investissement: Brief van de Fondsbeheerder

Belangrijke wettelijke informatie

Reclame. Raadpleeg het document essentiële beleggersinformatie /prospectus voordat u een beleggingsbeslissing neemt. Dit document is enkel bestemd voor professionele klanten en is niet gevalideerd door het FSMA.

Dit document is gepubliceerd door Carmignac Gestion S.A., een door de Franse toezichthouder Autorité des Marchés Financiers (AMF) erkende vermogensbeheerder, en zijn Luxemburgse dochteronderneming, Carmignac Gestion Luxembourg, S.A., een door de Luxemburgse toezichthouder Commission de Surveillance du Secteur Financier (CSSF) krachtens artikel 15 van de Luxemburgse wet van 17 december 2010 erkende beheermaatschappij van beleggingsfondsen. "Carmignac" is een gedeponeerd merk. "Investing in your Interest" is een aan het merk Carmignac verbonden slogan.

Dit document vormt geen advies met het oog op een belegging in of arbitrage van effecten of enig ander beheer- of beleggingsproduct of enige andere beheer- of beleggingsdienst. De in dit document opgenomen informatie en meningen houden geen rekening met de specifieke individuele omstandigheden van de belegger en mogen in geen geval worden beschouwd als juridisch, fiscaal of beleggingsadvies. De informatie in dit document kan onvolledig zijn en kan ook zonder voorafgaande kennisgeving worden gewijzigd. Dit document mag noch geheel noch gedeeltelijk worden gereproduceerd zonder voorafgaande toestemming.

In het verleden behaalde resultaten zijn geen garantie voor de toekomst. De resultaten zijn netto na aftrek van kosten (inclusief mogelijke in rekening gebrachte instapkosten door de distributeur) . Nettorendementen worden berekend na aftrek van de van toepassing zijnde kosten en belastingen voor een gemiddelde retailclient die een fysiek Belgisch ingezetene is.

Als gevolg van wisselkoersschommelingen kan het rendement van aandelenklassen waarvan het wisselkoersrisico niet is afgedekt, stijgen of dalen.

Verwijzingen naar bepaalde waarden of financiële instrumenten zijn voorbeelden van beleggingen die in de portefeuilles van de fondsen van Carmignac aanwezig zijn of waren. Deze verwijzingen hebben niet tot doel om directe beleggingen in die instrumenten aan te moedigen en zijn geen beleggingsadvies. De Beheermaatschappij is niet onderworpen aan het verbod op het uitvoeren van transacties met deze instrumenten voorafgaand aan de verspreidingsdatum van de informatie. De portefeuilles van de fondsen van Carmignac kunnen op ieder moment worden gewijzigd.

De verwijzing naar een positionering of prijs, is geen garantie voor de resultaten in de toekomst van de UCIS of de manager.

Risicocategorie van het KID (Essentiële Informatiedocument) indicator. Risicocategorie 1 betekent niet dat een belegging risicoloos is. Deze indicator kan in de loop van de tijd veranderen.

De aanbevolen beleggingshorizon is een minimale horizon en geen aanbeveling om uw beleggingen aan het einde van deze periode te verkopen.

Morningstar Rating™ : © Morningstar, Inc. Alle rechten voorbehouden. De informatie in dit document is eigendom van Morningstar en/of zijn informatie leveranciers, mag niet gekopieerd of verspreid worden en wordt niet gegarandeerd als zijnde exact, volledig of geschikt op dit moment. Morningstar noch zijn informatieleveranciers zijn verantwoordelijk voor eventuele schade of verliezen als gevolg van het gebruik van deze informatie.

Bij de beslissing om in het gepromote fonds te beleggen moet rekening worden gehouden met alle kenmerken of doelstellingen ervan zoals beschreven in het prospectus. De risico’s, beheerkosten en lopende kosten worden beschreven in de KID (Essentiële Informatiedocument). De prospectussen, de documenten met essentiële beleggersinformatie en de meest recente (half)jaarverslagen zijn kosteloos verkrijgbaar in het Nederlands en het Frans bij de beheermaatschappij, per telefoon op het nummer +352 46 70 60 1, op de website www.carmignac.be of bij Caceis Belgium S.A., de vennootschap die de financiële dienstverlening in België verzorgt, op het adres Havenlaan 86c b320, B-1000 Brussel. De essentiële beleggersinformatie moet vóór elke inschrijving worden verstrekt aan de belegger, welke door de belegger vóór elke inschrijving gelezen moet worden. Dit fonds mag direct noch indirect aangeboden of verkocht worden ten gunste of voor rekening van een 'U.S. person', zoals gedefinieerd in de Amerikaanse 'Regulation S' en de FATCA. De netto-inventariswaarde zijn beschikbaar op de website www.fundinfo.com. Elke klacht kan worden gestuurd naar complaints@carmignac.com of naar CARMIGNAC GESTION – Compliance and Internal Controls – 24 place Vendôme Paris France of op de website www.ombudsfin.be.

Indien u inschrijft op een GBF (gemeenschappelijk beleggingsfonds) naar Frans recht, moet u uw deel van de door het fonds ontvangen dividenden (en, in voorkomend geval, interesten) elk jaar op uw belastingaangifte vermelden. U kunt een gedetailleerde berekening maken op www.carmignac.be. Deze rekenmodule is geen belastingadvies, maar uitsluitend een hulpmiddel voor de berekening. Dit ontslaat u niet van de zorgvuldigheid en de controles waartoe u als belastingplichtige gehouden bent. De getoonde resultaten zijn gebaseerd op door u verstrekte gegevens. Carmignac kan in geen geval aansprakelijk worden gesteld voor fouten of nalatigheden uwerzijds.

Wanneer beleggers inschrijven op een fonds dat onder de spaarrichtlijn valt, moeten zij overeenkomstig artikel 19bis van CIR92 bij de inkoop van hun aandelen een roerende voorheffing van 30% betalen op de inkomsten die in de vorm van rente, meerwaarden of minderwaarden voortvloeien uit de opbrengst van in schuldbewijzen belegde activa. De uitkeringen zijn onderworpen aan de roerende voorheffing van 30% zonder inkomen onderscheid.

Carmignac Portfolio verwijst naar de subfondsen van Carmignac Portfolio SICAV, een beleggingsmaatschappij naar Luxemburgs recht die voldoet aan de ICBE-richtlijn. De Fondsen zijn beleggingsfondsen in contractuele vorm (FCP) conform de UCITS-richtlijn of AFIM-richtlijn onder Frans recht.

De beheermaatschappij kan de verkoop in uw land op elk moment stopzetten. Beleggers kunnen via de volgende link toegang krijgen tot een samenvatting van hun rechten in het Frans, of het Nederlands in deel 6 zonder de titel Samenvatting van de beleggersrechten.