Driemaandelijkse Verslag

Carmignac P. EM Debt: Letter from the Fund Manager

-

+1.97%Carmignac P. EM Debt’s performance

in the 2nd quarter of 2023 for the FW EUR Share class

-

+2.08%Reference indicator¹’s performance

in the 2nd quarter of 2023 for JP Morgan GBI – Emerging Markets Global Diversified Composite Unhedged EUR Index

-

+6.37%3-year annualized performance

versus -0.46% for the reference indicator over the period

Carmignac P. EM Debt gained +1.97% in the second quarter of 2023, while its reference indicator1 was up +2.08%.

Market environment

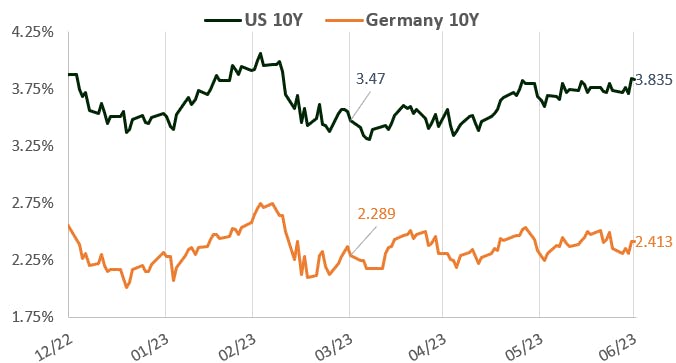

The second quarter has been characterized by strong bullish sentiment in risky markets as well as higher global rates. The 10-year Treasury went from around 3.5% to over 3.8%, while the MSCI World added 3.7% of performance.

Germany and US 10-year rates evolution

Sources: Carmignac, Bloomberg, 30/06/2023

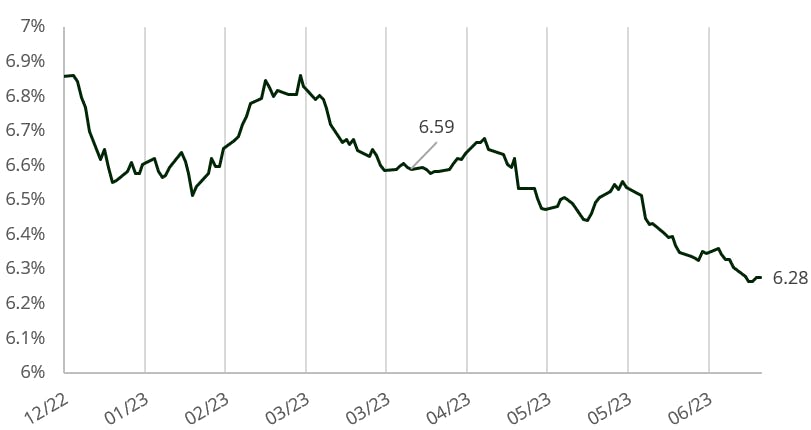

In terms of local rates, we have continued to see a slowdown in the emerging market (EM) inflation (as well as developed markets (DM) inflation). In this context the local bonds performed particularly well with the reference indicator GBI-EM index’s yield dropping by 31 basis points over the quarter. We also saw the first rate cut in the EM universe this quarter with Hungary cutting twice by 100bps each time its overnight rate. We think that a number of countries are likely to follow in the next 2 quarters, such as Brazil, Chile, and Czechia.

GBI-EM Index (Local sovereign debt index) - Yield Evolution

Sources: Carmignac, Bloomberg, 30/06/2023

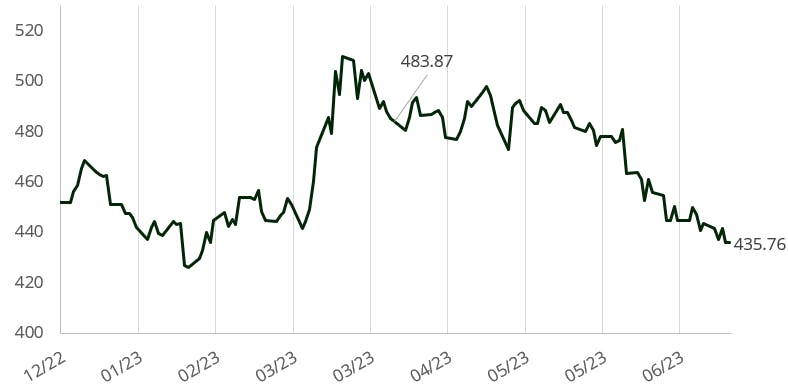

Furthermore FX, despite the lower rates in EM retained a strong real carry and continued to attract investors with the exception of Asia suffering from its negative carry. We also saw that the political noise in Israel and South Africa (as well as power issues) significantly affected these currencies. For the sovereign credit we have seen a good performance with the EMBIGD1 index as a whole, but the EMBIGD HY2 outperformed with a compression of spreads by 60bps over the period.

J.P Morgan EMBIG diversified hedged EURO index (External sovereign debt index) - Spread Evolution

Sources: Carmignac, Bloomberg, 30/06/2023

What have we done in this context?

In this context we have benefitted from the Local Rates rally in the CZK, HUF, MXN and BRL curves. Following the rally, we started to reduce as large interest rate cuts are starting to get priced, and the usual correlation between DM rates and these Local Curves seems to have broken during this quarter. In particular we have reduced the CZK, BRL and MXN rates. In the FX space we continue to enjoy the carry and performance of EM FX currencies. Like in the previous quarter we have been long HUF, CZK, BRL, and MXN. During the quarter we reduced our HUF after its strong rally and as the central bank started to cut rates at a steep pace. We also used the weakness in ILS and ZAR to enter into tactical positions. For sovereign credit, following the strong performance of the high yield (HY) we took the chance to reduce the exposure of the fund while keeping our more investment grade (IG) names. Another important event was our purchase of Turkey credit default swap (CDS) to protect the book but which paid off as Erdogan won the elections where we also reduced the protection.

Outlook for the next months

Looking forward to it, we still expect a recession to hit the global economy: high rates are eating at demand and effect we are already largely seeing it in the EM world. Furthermore, China which last quarter was seen as launching a potentially large stimulus to boost growth, is showing that it is unwilling to repeat the policies of the past thus removing a possible source of global growth. This view of recession and high rates is reflected in our portfolio construction, namely a large reduction of risk assets. We also remain focused on duration with the view that a recession would force DM central banks to cut rates and thus enable further cuts in the EM world. This leaves us with EM FX which offer carry while having a central bank ready to defend the currency such as the CZK and the INR, as well as tactical/opportunist investments. In Local Rates we are ready to re-engage in the hikers notably in the BRL or HUF once the FED or ECB have paused and EM central banks can accelerate their cutting cycles. In Credit we remain cautious with protection against our HY names and will keep our positioning light and focused on the IG space.

1 J.P Morgan EMBIG diversified hedged EURO index

2 J.P Morgan EMBIG HY diversified hedged EURO index

Carmignac Portfolio EM Debt FW EUR Acc

Het indicator kan variëren van 1 tot 7, waarbij categorie 1 overeenkomt met een lager risico en een lager potentieel rendement, en categorie 7 met een hoger risico en een hoger potentieel rendement. De categorieën 4, 5, 6 en 7 impliceren een hoge tot zeer hoge volatiliteit, met grote tot zeer grote prijsschommelingen die op korte termijn tot latente verliezen kunnen leiden.

Aanbevolen minimale beleggingstermijn

Laagste risico Hoogste risico

Risico's die in de indicator niet voldoende in aanmerking worden genomen:

KREDIETRISICO: Het kredietrisico stemt overeen met het risico dat de emittent haar verplichtingen niet nakomt.

TEGENPARTIJRISICO: Risico van verlies indien een tegenpartij niet aan haar contractuele verplichtingen kan voldoen.

RISICO VERBONDEN AAN BELEGGINGEN IN CHINA: Specifieke risico's verbonden aan het gebruik van het platform Hong-Kong Shanghai Connect en andere risico's verbonden aan beleggingen in China.

LIQUIDITEITSRISICO: Risico dat tijdelijke marktverstoringen de prijzen beïnvloeden waartegen een ICBE zijn posities kan vereffenen, innemen of wijzigen.

Inherente risico's:

OPKOMENDE LANDEN : De netto-inventariswaarde van het compartiment kan sterk variëren vanwege de beleggingen in de markten van de opkomende landen, waar de koersschommelingen aanzienlijk kunnen zijn en waar de werking en de controle kunnen afwijken van de normen op de grote internationale beurzen.

RENTERISICO: Renterisico houdt in dat door veranderingen in de rentestanden de netto-inventariswaarde verandert.

WISSELKOERS: Het wisselkoersrisico hangt samen met de blootstelling, via directe beleggingen of het gebruik van valutatermijncontracten, aan andere valuta’s dan de waarderingsvaluta van het Fonds./size]

KREDIETRISICO: Het kredietrisico stemt overeen met het risico dat de emittent haar verplichtingen niet nakomt.

RISICO VAN KAPITAALVERLIES: Dit deelbewijs/deze aandelenklasse biedt geen garantie voor of bescherming van het belegde kapitaal. U ontvangt mogelijk niet het volledige belegde bedrag terug.

Meer informatie over de risico's van het deelbewijs/de aandelenklasse is te vinden in het prospectus, met name in hoofdstuk "Risicoprofiel", en in het document met essentiële beleggersinformatie.

Carmignac Portfolio EM Debt FW EUR Acc

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2024 (YTD) ? Year to date |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Carmignac Portfolio EM Debt FW EUR Acc | - | - | - | +1.10 % | -9.97 % | +28.88 % | +10.54 % | +3.93 % | -9.05 % | +15.26 % | -0.06 % |

| Referentie-indicator | - | - | - | +0.42 % | -1.48 % | +15.56 % | -5.79 % | -1.82 % | -5.90 % | +8.89 % | -0.82 % |

Scroll rechts om de volledige tabel te zien

| 3 jaar | 5 jaar | 10 jaar | |

|---|---|---|---|

| Carmignac Portfolio EM Debt FW EUR Acc | +2.49 % | +8.02 % | - |

| Referentie-indicator | +0.94 % | +0.72 % | - |

Scroll rechts om de volledige tabel te zien

Bron: Carmignac op 30/04/2024

| Instapkosten : | Wij brengen geen instapkosten in rekening. |

| Uitstapkosten : | Wij brengen voor dit product geen uitstapkosten in rekening. |

| Beheerskosten en andere administratie - of exploitatiekos ten : | 1,05% van de waarde van uw belegging per jaar. Dit is een schatting op basis van de feitelijke kosten over het afgelopen jaar. |

| Prestatievergoedingen : | Er is geen prestatievergoeding voor dit product. |

| Transactiekosten : | 0,57% van de waarde van uw belegging per jaar. Dit is een schatting van de kosten die ontstaan wanneer we de onderliggende beleggingen voor het product kopen en verkopen. Het feitelijke bedrag zal varieert naargelang hoeveel we kopen en verkopen. |