Fondsen Focus

Carmignac P. Unconstrained Credit: the Fund Manager's thought

In the third quarter of 2020, Carmignac Portfolio Unconstrained Credit posted a performance of +4.12% versus a +2.14% gain for its reference indicator, generating a +1.98% outperformance. For the first nine months of the year, the Fund returned a performance of +4.30%, while its reference indicator is down -0.02%.

Life is far from having gotten back to what it was before Covid 19, but the third quarter of 2020 was much closer to normality than the first half of the year. This is also true for credit markets which, gradually, are becoming driven again by the long term trend which had prevailed for the past years: investors are anxious, fearful of credit accidents (be it downgrades or defaults) while an abundance of capital remains allocated to the asset class.

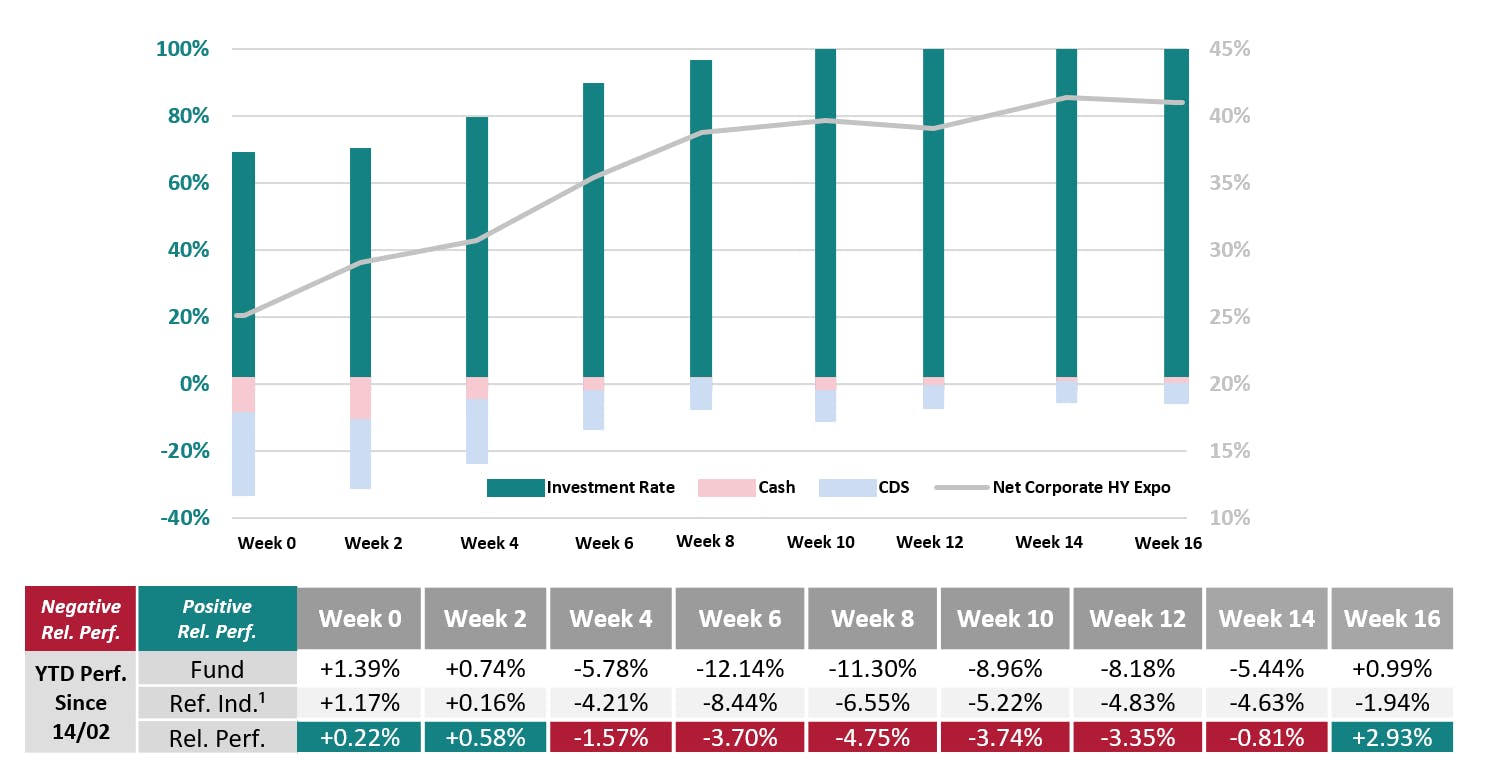

Managing Carmignac P. Unconstrained Credit Through a Market Dislocation (%)

Source: Carmignac as at 05/06/2020. A EUR Share class ¹75% ICE BofA Euro Corporate Index (ER00) and 25% ICE BofA Euro Hight Yield Index (HE00) calculated with coupons reinvested and rebalanced quarterly.Past performance is not necessarily indicative of future performance.The return may increase or decrease as a result of currency fluctuations. Performance are net of fees(excluding applicable entrance fee qcuired to the distributor)¹CCR= Carmignac P. Unconstrained Cred,*CDS=Credit Default Swap.

This environment bears a lot of similarities with the first half of 2016 or, closer to us, the first half of 2019. We expect the coming months to be similarly fertile for bond pickers. This is not to say it will be a smooth or easy ride. We are already seeing a sharp rise in credit rating downgrades and defaults and we expect more accidents in the next quarters.

-

Central bankers can help sound businesses refinance themselves and pay lower interest expenses but they cannot save disrupted, structurally unprofitable business models. It is often said that defaults are caused by the economic environment. While there is a correlation, we do not believe there is much causality. Issuers rarely default on their debt because GDP growth turned out one or two percentage points lower than expected.

-

They default because their business models have been disrupted or competed away and/or because investors have not been careful in their due diligence and analysis when assessing how much debt they can bear.

Recessions only lower the willingness and ability to kick the can down the road. Hence, the measures taken to fight Covid19 will have an important impact on default rates but there would have had a high occurrence of defaults in the coming years even without this virus. It will mostly act as a catalyst, precipitating defaults which would have occurred in two or three years.

This is why we always keep in perspective the multiyear outlook of a full credit cycle when picking investments and deciding how much risk we want to put in the portfolio - while credit markets tend to price only short-term default rates, which is akin to driving a motorbike looking only one meter in front of the handlebar.

We are excited by the opportunities we see ahead. During the past months, the fund has benefited from high quality credit repricing to a more normal level. Yet we still have in our portfolio many bonds from solid businesses with sound business models, good balance sheets and continuous access to liquidity, yielding far in excess than their fundamental cost of risk, even under the assumption of a painfully slow economic recovery.

We also see a lot of excess spread in Collateralized Loan Obligations (“CLOs) tranches, with very limited fundamental risk - we would need much more pessimistic assumptions to break those tranches than what is needed to break other asset classes. As a result, we believe the risk-adjusted yield of the fund is very attractive at the moment. Beyond our current portfolio, as we wrote above, we expect the upcoming wave of accidents will keep risk aversion high and create numerous investment opportunities, long and short.

Carmignac Portfolio Credit A EUR Acc

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2024 (YTD) ? Year to date |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Carmignac Portfolio Credit A EUR Acc | - | - | - | +1.79 % | +1.69 % | +20.93 % | +10.39 % | +2.96 % | -13.01 % | +10.58 % | +2.51 % |

| Referentie-indicator | - | - | - | +1.13 % | -1.74 % | +7.50 % | +2.80 % | +0.06 % | -13.31 % | +9.00 % | +0.70 % |

Scroll rechts om de volledige tabel te zien

| 3 jaar | 5 jaar | 10 jaar | |

|---|---|---|---|

| Carmignac Portfolio Credit A EUR Acc | +0.09 % | +5.12 % | - |

| Referentie-indicator | -1.58 % | +0.30 % | - |

Scroll rechts om de volledige tabel te zien

Bron: Carmignac op 28/03/2024

| Instapkosten : | 2,00% van het bedrag dat u betaalt wanneer u in deze belegging instapt. Dit is het hoogste bedrag dat u in rekening zal worden gebracht. Carmignac Gestion rekent geen instapkosten. De persoon die u het product verkoopt, informeert u over de daadwerkelijke kosten. |

| Uitstapkosten : | Wij brengen voor dit product geen uitstapkosten in rekening. |

| Beheerskosten en andere administratie - of exploitatiekos ten : | 1,20% van de waarde van uw belegging per jaar. Dit is een schatting op basis van de feitelijke kosten over het afgelopen jaar. |

| Prestatievergoedingen : | 20,00% wanneer de aandelenklasse tijdens de prestatieperiode beter presteert dan de referentie-indicator. Het zal ook worden betaald als de aandelenklasse beter heeft gepresteerd dan de referentie-indicator, maar een negatieve prestatie had. Ondermaatse prestaties worden voor 5 jaar teruggevorderd. Het werkelijke bedrag hangt af van hoe goed uw belegging presteert. De geaggregeerde kostenraming hierboven omvat het gemiddelde over de laatste 5 jaar, of sinds de creatie van het product als dit minder dan 5 jaar is. |

| Transactiekosten : | 0,43% van de waarde van uw belegging per jaar. Dit is een schatting van de kosten die ontstaan wanneer we de onderliggende beleggingen voor het product kopen en verkopen. Het feitelijke bedrag zal varieert naargelang hoeveel we kopen en verkopen. |

* Reference Indicator: 75% ICE BofA Euro Corporate Index (ER00) and 25% ICE BofA Euro High Yield Index (HE00) calculated with coupons reinvested and rebalanced quarterly. 2017 Performance : since the launch of the fund on 31/07/2017. Performance of the A EUR acc share class. Past performance is not necessarily indicative of future performance. The return may increase or decrease as a result of currency fluctuations. Performances are net of fees (excluding possible entrance fees charged by the distributor).

Carmignac Portfolio Credit A EUR Acc

Het indicator kan variëren van 1 tot 7, waarbij categorie 1 overeenkomt met een lager risico en een lager potentieel rendement, en categorie 7 met een hoger risico en een hoger potentieel rendement. De categorieën 4, 5, 6 en 7 impliceren een hoge tot zeer hoge volatiliteit, met grote tot zeer grote prijsschommelingen die op korte termijn tot latente verliezen kunnen leiden.

Aanbevolen minimale beleggingstermijn

Laagste risico Hoogste risico

Risico's die in de indicator niet voldoende in aanmerking worden genomen:

KREDIETRISICO: Het kredietrisico stemt overeen met het risico dat de emittent haar verplichtingen niet nakomt.

TEGENPARTIJRISICO: Risico van verlies indien een tegenpartij niet aan haar contractuele verplichtingen kan voldoen.

RISICO VERBONDEN AAN BELEGGINGEN IN CHINA: Specifieke risico's verbonden aan het gebruik van het platform Hong-Kong Shanghai Connect en andere risico's verbonden aan beleggingen in China.

LIQUIDITEITSRISICO: Risico dat tijdelijke marktverstoringen de prijzen beïnvloeden waartegen een ICBE zijn posities kan vereffenen, innemen of wijzigen.

Inherente risico's:

RENTERISICO: Renterisico houdt in dat door veranderingen in de rentestanden de netto-inventariswaarde verandert.

KREDIETRISICO: Het kredietrisico stemt overeen met het risico dat de emittent haar verplichtingen niet nakomt.

VALUTARISICO: Het wisselkoersrisico hangt samen met de blootstelling, via directe beleggingen of valutatermijncontracten, aan andere valuta’s dan de waarderingsvaluta van de ICBE.

RISICO IN VERBAND MET HET GEBRUIK VAN DERIVATEN: deze producten gaan gepaard met specifieke risico's van verlies.

RISICO VAN KAPITAALVERLIES: Dit deelbewijs/deze aandelenklasse biedt geen garantie voor of bescherming van het belegde kapitaal. U ontvangt mogelijk niet het volledige belegde bedrag terug.

Meer informatie over de risico's van het deelbewijs/de aandelenklasse is te vinden in het prospectus, met name in hoofdstuk "Risicoprofiel", en in het document met essentiële beleggersinformatie.